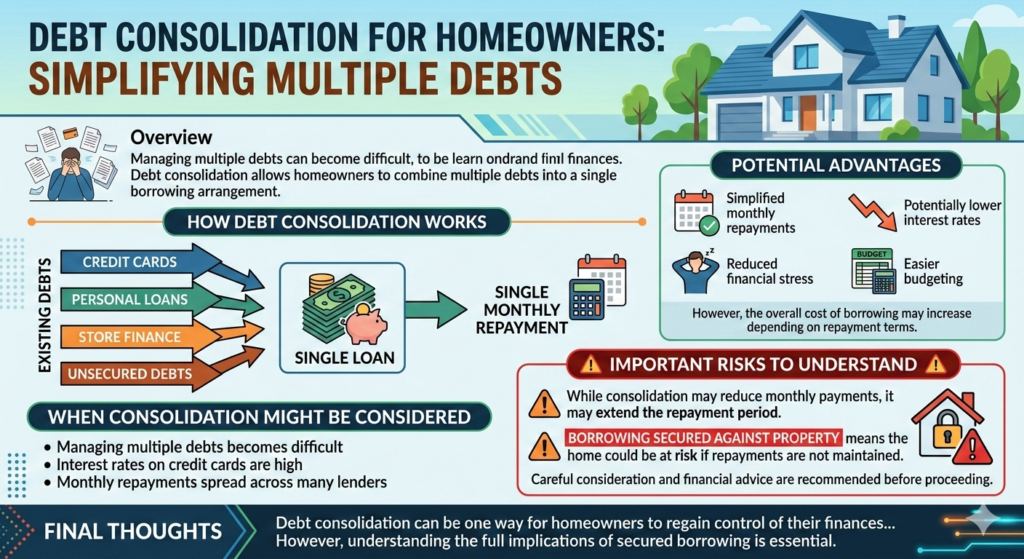

Overview

Managing multiple debts can become difficult over time, particularly when repayments are spread across several lenders. Debt consolidation allows homeowners to combine multiple debts into a single borrowing arrangement.

For some homeowners, consolidating debts secured against property may reduce monthly payments and simplify financial management.

How debt consolidation works

Debt consolidation replaces several existing debts with a single loan.

This can include combining:

- Credit card balances

- Personal loans

- Store finance agreements

- Other unsecured debts

Instead of managing several repayments, homeowners make a single monthly payment.

Potential advantages

Debt consolidation can offer several potential benefits.

These may include:

- Simplified monthly repayments

- Potentially lower interest rates

- Reduced financial stress

- Easier budgeting

However, the overall cost of borrowing may increase depending on repayment terms.

When consolidation might be considered

Homeowners may explore consolidation when:

- Managing multiple debts becomes difficult

- Interest rates on credit cards are high

- Monthly repayments are spread across many lenders

Consolidating debts secured against property can sometimes reduce short-term financial pressure.

Important risks to understand

While consolidation may reduce monthly payments, it may extend the repayment period.

Borrowing secured against property means the home could be at risk if repayments are not maintained.

Careful consideration and financial advice are recommended before proceeding.

Final thoughts

Debt consolidation can be one way for homeowners to regain control of their finances by simplifying multiple repayments.

However, understanding the full implications of secured borrowing is essential before making any financial commitments.

admin

admin